HUGE INSIGHTS: The Big Picture - Issue #30

The Year of Living Dangerously

Please enjoy the free portion of this monthly newsletter with our compliments. To get full access, you might want to consider an upgrade to paid for as little as $12.50/month. As an added bonus, paid subscribers also receive our weekly ALPHA INSIGHTS: Idea Generator Lab publication, which details our top actionable trade idea and provides updated market analysis every Wednesday, as well as other random perks, including periodic ALPHA INSIGHTS: Interim Bulletin reports and quarterly video content.

Executive Summary

Thinking in Bets

2024 Election: Misdirection or Disconnection?

Labor Pains

Geopolitical Perspective: Year of the Dragon

Market Analysis & Outlook: Don’t Forget Rule #7

Conclusions & Positioning: Some Healthy Advice

Thinking in Bets

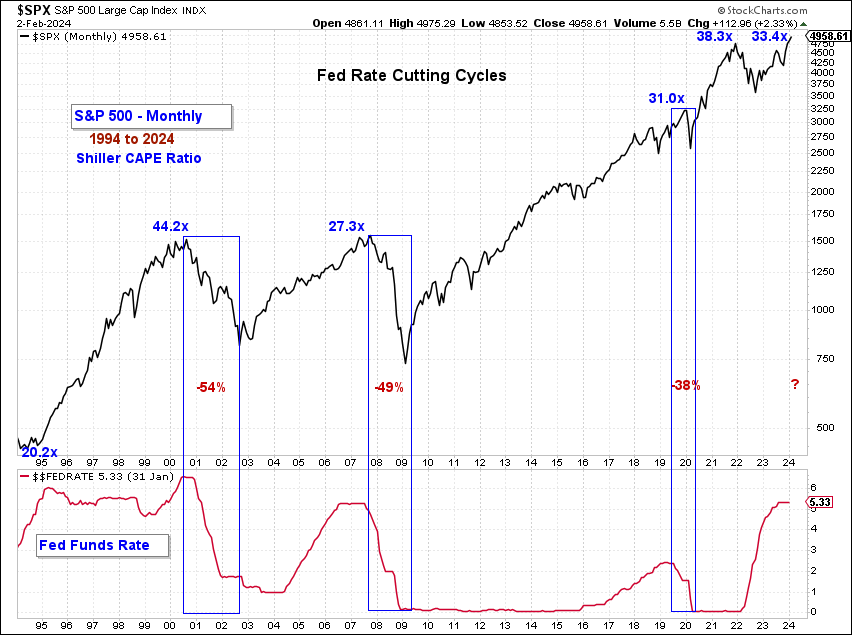

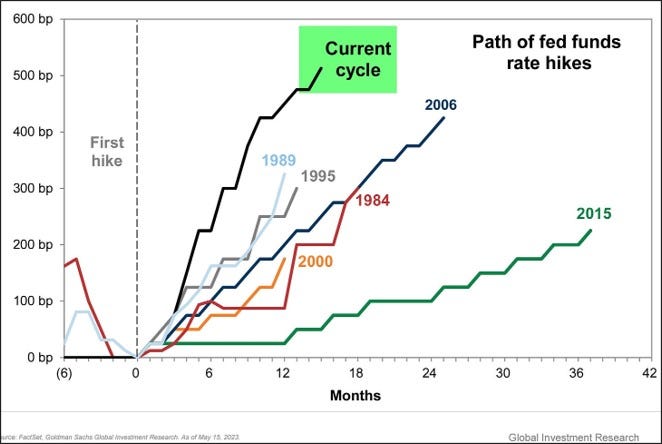

There is a very large bet on the table. Market participants have universally embraced the logic presented by Federal Reserve Chairman Jerome Powell, that growth and employment trends remain strong, while inflation has subsided. Powell and company have taken their foot off the brake for now and have been coasting for the past four FOMC meetings. Moreover, a number of the committee’s members have vocally endorsed the expectation that the Fed may soon move their foot to the accelerator, penning in as many as three 25 bps rate cuts before year-end. And like all good chess players, savvy market participants are attempting to look several moves deeper into the board, and by extrapolating the trend of the latest data forward, they have collectively concluded that at least five 25 bps cuts are more likely before year-end, beginning as soon as the May 1st FOMC meeting as of this writing.

The problem with this approach is that we live in an uncertain world. As such, we are forced to make decisions when we don’t have all of the facts. Even the Fed doesn’t have all the information necessary to make consistently correct policy judgements — as they have woefully demonstrated time and again. Indeed, according to Annie Duke, author, cognitive-behavioral decision science expert, and winner of the 2004 World Series of Poker Tournament of Champions, life is much more like poker than chess. While chess is a highly strategic game that requires skill, in Duke’s view, it’s unlike life in that it involves very little hidden information or luck. “Poker, on the other hand, is a much better model for life because it combines skill, luck, and decision making in the face of incomplete information. In chess, if you make all of the right decisions, you’re likely to win, whereas in poker, that’s not the case.” In her bestselling book, Thinking in Bets, the Duchess of Poker draws on examples from business, sports and politics to demonstrate how the outcome of our decisions oftentimes has little to do with the quality of our decisions. Good decisions can have bad outcomes, and vice versa.

Case and point, Duke illustrates that in Super Bowl XLIX, Seattle Seahawks coach Pete Carroll made one of the most controversial calls in football history: With 26 seconds remaining, and trailing by four at the Patriots’ one-yard line, he called for a pass instead of a hand off to his star running back — Marshawn Lynch. The pass was intercepted and the Seahawks lost. Critics called it the dumbest play in history. “But was the call really that bad?” Duke asks, “Or did Carroll actually make a great move that was ruined by bad luck?” Despite an onslaught of headlines to the contrary, Brian Burke of Slate.com and Benjamin Morris of FiveThirtyEight.com both defended Carroll’s decision to throw the ball, citing a mere 2 percent probability of an interception in that situation based upon the past fifteen seasons of play. Duke points out that, “Carroll had control of the play-call decision, but he had no control over how it turned out.” Objectively, he called a play that had a high probability of ending in either a game-winning touchdown or an incomplete pass, in which case it would have allowed time for two more plays for the Seahawks to hand off the ball to Marshawn Lynch — the play that Belichick and the Patriots were expecting all along. As Duke puts it, “He made a good-quality decision that got a bad result.”

Similarly, the Fed also has control over the play-call decision with respect to monetary policy, but no control over how it will turn out. So, assuming that the Fed is on track to make a good-quality policy decision — as market participants currently presume, what could potentially go wrong? To be sure, market participants simply may not have all of the facts. Their bullish sentiment and positioning suggests that they assume the Fed’s abrupt shift from hawkish to dovish rhetoric at the December FOMC meeting signals high confidence in a so-called “soft landing” — a scenario whereby the economy avoids recession as growth stabilizes very near potential, while employment remains strong and core inflation achieves the Fed’s 2.0% target.

But what if the Fed’s true motivation to transition away from their current restrictive policy stance is because they see emerging risks to economic growth and rising evidence of a deterioration in employment trends? What if the Fed actually recognizes that they have been wrong 78% of the time, and that 11 of the past 14 rate hike cycle since 1957 have ended in recession? We are now nearly 23 months past the first rate hike. What if the Fed knows that the long and variable lags to monetary policy’s impact on the economy work in both directions, and that the average time from the first rate hike to the start of a recession is 26 months? The fact of the matter is, that following the most severe monetary policy tightening campaign in over 40 years, no one — including and especially the Fed — knows exactly how long it will take for the effect of higher interest rates to fully flow through the economy. The English writer, philosopher, and theologian G.K. Chesterton once wrote, “The real trouble with this world of ours is not that it is an unreasonable world, nor even that it is a reasonable one. The commonest kind of trouble is that it is nearly reasonable, but not quite. Life is not an illogicality; yet it is a trap for logicians. It looks just a little more mathematical and regular than it is; its exactitude is obvious, but its inexactitude is hidden; its wildness lies in wait.”

One potential example of this hidden inexactitude may soon be poised to reveal itself. Quantitative tightening (QT), the process whereby the Federal Reserve reduces its holdings of U.S. Treasury securities by allowing them to run-off the balance sheet (i.e. mature without reinvesting the proceeds), thus removing liquidity from the financial system, has been determined to be nearing the end of its useful life, such that the Fed is now considering terminating the policy. With over $7.6 trillion in U.S. Treasury debt maturing over the next 12-months and an estimated $2 trillion in new issuance needed to fund a growing fiscal budget deficit, the Fed must now balance the liquidity needs of the Treasury with the liquidity needs of the banking system. According to research from the Brooking Institute, the end of QT is likely to occur in 1Q25. However, the aggressive drawdown in the Overnight Reverse Repurchase (ON RRP) facility from $2.2 trillion in May of last year to just $503 billion today (mainly due to money market funds’ preference for slightly higher yielding T-bills), leaves total bank reserves at a mere $3.7 trillion as of January 18th, 2024.

The Fed’s official policy is for the banking system to maintain so-called “ample” reserves — or about 10% to 12% of nominal GDP according to St. Louis Fed President Christopher Waller (an estimated $2.7 trillion to $3.4 trillion based upon 2023 GDP data). Reserves are currently considered to be “abundant,” so a further drawdown to zero in the ON RRP facility should not (in theory) upset the apple cart. That being said, the 2019 episode shows the challenge the Fed faces in figuring out just how ample reserves are. As the Fed shrank its balance sheet from October 2014 to September 2019, the level of bank reserves fell to around $1.5 trillion. At the time, the Fed believed that would leave the banking system with sufficiently ample reserves. That view proved wrong, as the Fed learned when short-term rates in money markets shot up in September 2019 and banks held onto reserves instead of using them to lend at attractive interest rates. In response to that miscalculation, the Fed had to abruptly reverse course, and again begin increasing reserves and the size of its balance sheet.

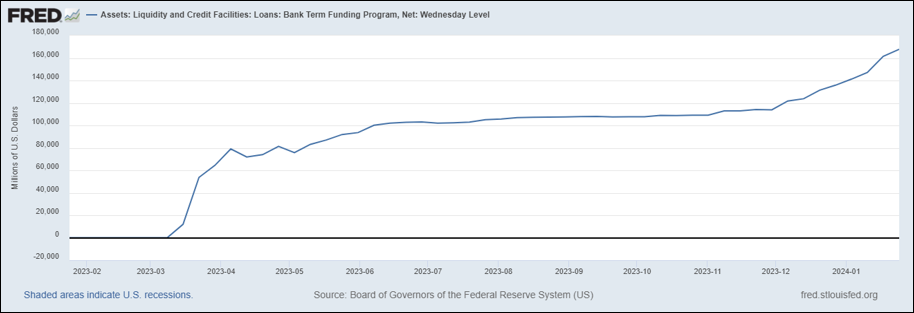

The latest twist in the puzzle has to do with the Fed’s 2023 emergency Bank Term Funding Program (BTFP), which was instituted in March 2023 following the regional banking crisis which consumed the likes of Silicon Valley Bank, First Republic Bank, and Signature Bank of NY. The BTFP was designed to be a temporary one-year back stop available to troubled banks so that they had access to adequate liquidity and time to reposition distressed HTM securities portfolios in an orderly manner. The BTFP is slated to end on March 11, 2024. Yet, as of January 24, 2024, the BTFP had reach a new record high of $167.8 billion in outstanding loans. If the Fed ends the program as scheduled, these borrowers will then be forced to go to the Fed’s discount window for funding at much higher rates and collateral requirements — not to mention the associated shame of it.

During the DoubleLine Round Table Prime 2024: Market Outlook, founder Jeffrey Gundlach posed an interesting question to the panel: What if everything we think we know about the markets, because of our experience over the past forty years, is informed solely by a secular decline in long-term interest rates? Today, everyone thinks they know how the system works, but what if we have now entered a new regime — a secular rise in interest rates?” Gundlach points out that prior to the GFC the U.S. fiscal budget deficit was about 3 percent of GDP. Following the GFC it went to 9 percent. Today, we’re running a deficit of over 6 percent — and these are presumably good times. So, if the U.S. economy were to enter recession, Gundlach suggests that, “there is every reason to believe that the federal budget deficit will go to at least 12 percent.” And if interest rates just backed-up to 6.0%, it would require 80% of tax receipts just to service our debt. “Maybe the Fed shouldn’t be so dogmatic about the inflation rate,” says Gundlach, “Maybe Jay Powell should more worried about solvency — of the entire financial system.” And to that, we say — maybe he is! The following sentence was struck from the January 31st FOMC policy statement, “The U.S. banking system is sound and resilient.” Was it removed because the resilience of the banking system is now so obvious to all that it’s no longer necessary to point it out? Or, was it removed as a hedge?

According to the Fed’s quarterly Senior Loan Officers Opinion Survey (SLOOS) more than one-third of those surveyed during the fourth quarter saw bank lending standards tightening (blue line). More importantly though, the growth of new commercial and industrial loans actually contracted during the month of December for the first time since 2008 — down -1.3% Y/Y (red line). This has never happened before in the history of the data without a concomitant U.S. economic recession. One reason why new commercial and industrial loan originations are contracting can be gleaned from a look at the Q4 results of New York Community Bancorp (NYCB).

Last Wednesday, the NYC commercial real estate lender posted a loss of -$0.29 vs. street expectations of a $0.27 profit. That constitutes a -193% negative earnings surprise. The shortfall owes largely to the $185 million in charge offs related to commercial loan defaults on a co-op property and an office property that the bank underwrote. This forced the bank’s management to slash its dividend by 70% and raise its loan loss reserve account to $552 million — or about 10x what was expected. The bank also noted that currently, the amount of loans that are between 30 and 90 days delinquent jumped by 48% in the final 3 months of 2023. NYCB’s stock price plunged -37% by the end of the day, and has continued to slide into the weekend. The news echoes that of early March 2023, when rumors of Silicon Valley Bank’s impending demise began circulating. The S&P Regional Banking ETF (KRE) is also under pressure — declining some -9% since the report. The consensus view is that this was an NYCB ‘specific’ problem associated with their purchase of the Signature Bank NY assets and not an industry-wide problem, but Wall Street analysts were truly stunned.

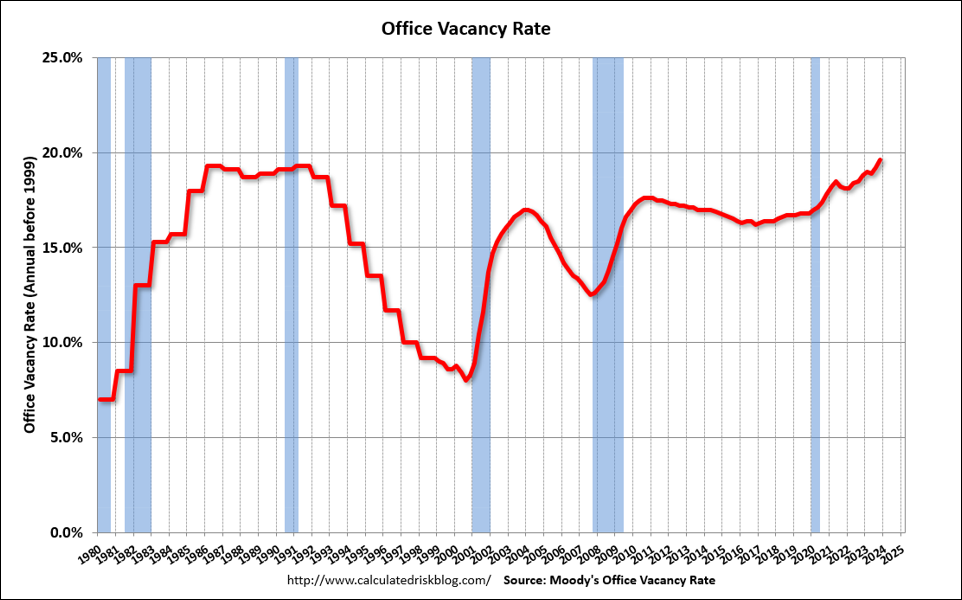

Billionaire Barry Sternlicht, chief executive officer of Starwood Capital Group, might disagree with the consensus. He sees more than $1 trillion of losses for office real estate. “The office market is in an existential crisis right now,” Sternlicht said last Tuesday at the iConnections Global Alts conference in Miami Beach. Once a $3 trillion asset class, offices now are “probably worth about $1.8 trillion,” he said. “There’s $1.2 trillion of losses spread somewhere, and nobody knows exactly where it all is.” Property owners have struggled to refinance loans as office building values have declined in the face of the highest vacancy rates in over four decades, while the Federal Reserve has been increasing interest rates sharply over the past two years. “Where regional banks had previously been a source of funds for real estate owners, they have disappeared from the market,” he said. “We’re in the business of getting loans,” continued Sternlicht. The banks “don’t show up, they’re not even playing. So the alternatives are the debt funds, which are having a field day.” The Fed’s policies have left a “serious mess in capital markets and real estate and anything that’s yield related,” he ranted. Sternlicht expects the first rate cut to come in June.

2024 Election: Misdirection or Disconnection?

Regardless of which party’s politics you prefer, the 2024 election process promises to be entertaining. As political junkies will know (among whom we are not), there are controversies developing within both major political parties.

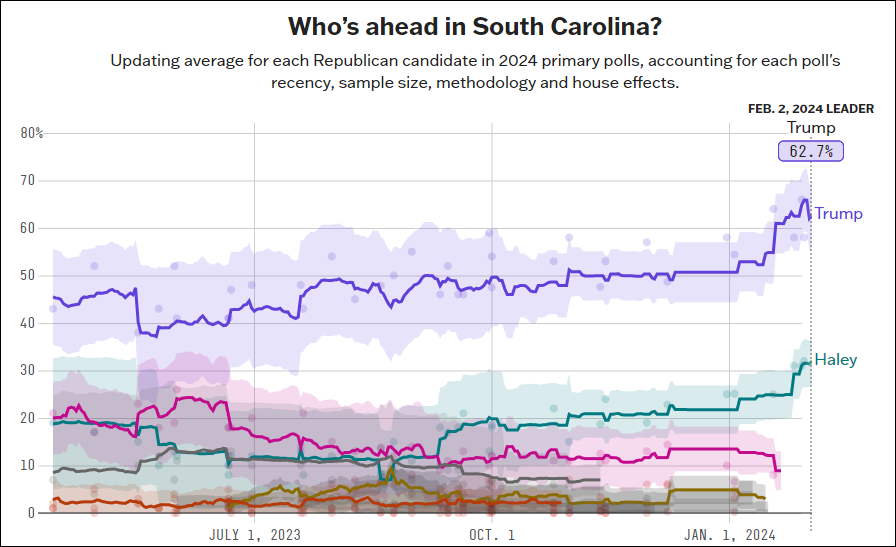

On the GOP side of the discussion, the embattled frontrunner, former President Donald Trump, has quickly cleared the field of all but one remaining challenger — former South Carolina Governor Nimarata “Nikki” Randhawa Haley. Trump recorded primary victories in both Iowa and New Hampshire, but with only slightly more than 50% of the vote. Can he take Haley in her home State? We’ll find out for certain on February 24th, but the path to a Haley nomination has gotten narrower to be sure. According to Nate Silver and the gang at FiveThirtyEight.com, Trump currently holds a solid 62.7% of the vote in South Carolina compared to Haley’s 32.1%.

On the Democratic party front, perhaps even more debatable is whether or not President Joe Biden will ultimately win the nomination. How could he lose an essentially uncontested race you ask? Allow us to explain. As some may be aware, there are rumblings within key inner circles of the Democratic party about Biden’s age, mental acuity, and general physical capacity to serve a second term as POTUS. Indeed, those rumblings are also beginning to question whether Biden could lose the 2024 election in a second face-off with Trump. Indeed, several possible replacement candidates have been floated including California Governor Gavin Newsome, Michigan Governor Gretchen Whitmer, and Illinois Governor Jay Pritzker to name a few. The fact that these potential candidates are even being discussed suggests that there is no confidence in Biden among the Democratic party elite. In a rare interview three weeks ago, on the Jay Shetty Podcast — On Purpose, former First Lady Michelle Obama expressed that she is “terrified” about the outcome of the upcoming 2024 presidential election. Could there be a backroom deal currently in negotiations for Biden to withdraw his candidacy from the race? Is it too late? Who would take his place and by what process could it be accomplished?

A New York Post article by Cindy Adams reports that former President Barack Obama has been polling donors to get their thoughts. Adams warned in the piece published on January 24th that Americans shouldn’t be shocked if Michelle Obama “sneaks her way into the race.” In the past, Mrs. Obama has been vocal about not ever running for public office. In fact, in her personal memoir, Becoming, the former First Lady was very clear that she had no desire to run for the Presidency. But in Adams’ column, she suggests that her sources tell her that the timeline to replace Biden has been accelerated from the long speculated Democratic National Convention in August, to as early as March — before Super Tuesday. To be sure, it would not be unprecedented. In 1968 President Lyndon Johnson withdrew from the race — albeit under very different circumstances. But is it too late for Mrs. Obama to get on the primary ballot in any State? Strictly speaking, yes. If Michelle Obama is to be the Democratic party’s candidate for President in 2024, the process would go something like this. First, the party’s superdelegates (unelected party elites) — who account for one-third of all the delegates — must endorse her. Then, Biden himself must agree to withdraw from the race and release his delegates, who presumably would in turn follow the superdelegates in endorsing Michelle Obama. In short, it is not impossible, but time is running out.

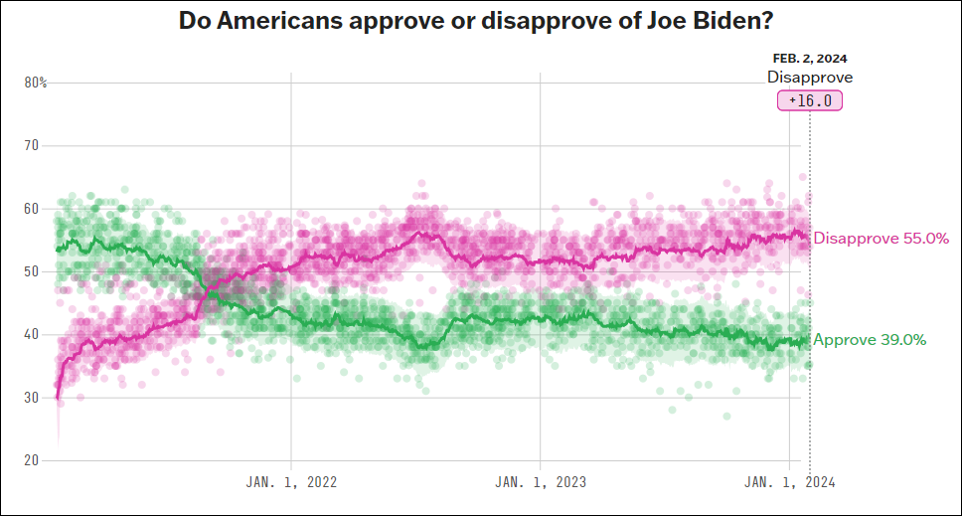

No doubt, a Donald Trump vs. Michelle Obama Presidential election battle would be interesting to say the least, if not immensely entertaining. Obviously, there is no guarantee that Biden will play ball. Then again, Biden’s current approval rating of just 39.0% is near the lows of his Presidency. Let the games begin!

Labor Pains

According to the Bureau of Labor Statistics (BLS), the U.S. economy added 353K non-farm jobs during the month of January, exceeding street expectations for an increase of 185K. This compared to an upwardly revised 333K in December and an upwardly revised 182K in November. It was the largest increase in monthly employment in the past year. On the other hand, the BLS made its annual benchmark revisions to earlier data, which added 359K jobs to 2023’s total gains — now averaging 255K per month last year vs. 225K before the revisions.

While this may sound impressive at the headline level, looking under the hood presents a different picture altogether. To begin, about one-third of the jobs created in January were non-productive jobs — Retail (45K), Government (36K), Social Assistance (30K), while productive segments of the economy lost 5K jobs. Indeed, according Quill Intelligence, 81% of the jobs created in 2023 were either in non-productive segments of the economy; were low-paying part-time or second jobs; or were accounted for as self-employment. Only 1% of the net new jobs created in 2023 were high-paying, full-time, white-collar jobs. In our view, despite a looming recession, the headline numbers will make the Fed’s job more difficult if they remain strong in the months ahead. Barring a financial calamity, we think the Fed will most likely come to the rescue too late — as usual.

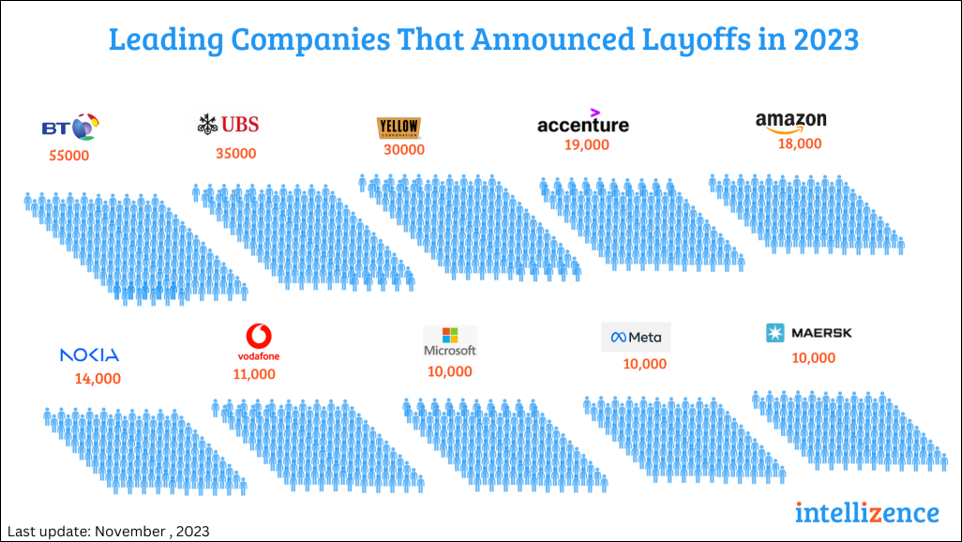

Moreover, layoffs in the middle ranks of corporate America are setting new records. Here are a few examples of companies that are leading the charge to cut headcount in recent months according to Intelligenze: