HUGE INSIGHTS: The Big Picture - Issue #32

HUGE INSIGHTS: The Big Picture - Issue #32

Into Thin Air

Please enjoy the free portion of this monthly newsletter with our compliments. To get full access, you might want to consider an upgrade to paid for as little as $12.50/month. As an added bonus, paid subscribers also receive our weekly ALPHA INSIGHTS: Idea Generator Lab publication, which details our top actionable trade idea and provides updated market analysis every Wednesday, as well as other random perks, including periodic ALPHA INSIGHTS: Interim Bulletin reports and video content.

Executive Summary

A View From the Top

A Prelude to Recession

Geopolitical Perspectives: To Russia with Love

Market Analysis & Outlook: Expect Change!

Conclusions & Positioning: Adventures in Energy

A View From the Top

We recently returned from an overseas excursion to New Zealand where we spent numerous hours hiking in the foothills of Aoraki/Mt. Cook, the place where Auckland-born Sir Edmund Hillary made his bones as a mountaineer and climber before summiting Mt. Everest with Tenzing Norgay in 1953. They were the first two climbers ever confirmed to have reached the world’s highest peak at 29,028 feet.

Hillary was then part of the ninth British expedition to Everest, led by John Hunt. At the time, the long-standing view among previous expeditions had been that the best climbing route to the summit of Everest was from the North slope — the Tibetan side of the mountain. But in 1949, China closed access to Mt. Everest from Tibet. That meant that the only other possibility would be to approach the summit from the South slope — controlled by Nepal. For the next several years, the government of Nepal allowed only one or two expeditions per year. In 1951, Hillary took part in a British reconnaissance expedition to Everest led by Eric Shipton. Shipton had been involved with most of the Everest expeditions since the 1930s and had climbed with Tenzing Norgay in a 1935 British reconnaissance expedition. In 1952, a Swiss expedition — in which Norgay took part — attempted to reach the summit, but was forced back just 800 feet below the peak due to bad weather and complications with oxygen sets. That same year, Hillary learned that he had been invited by Hunt to join the British summit attempt scheduled for the following year.

The 1953 expedition totalled over 400 people, including 362 porters, 20 Sherpa guides, and 10,000 pounds of gear and supplies. They set up base camp below the Khumbu Icefall in mid-March, and then slowly worked their way up to 25,900 feet to the South Col where they made their last camp. Hunt named two teams for the final ascent: Team one included Tom Bourdillon and Charles Evans; Team two included Hillary and Norgay. On May 26th, Bourdillon and Evans attempted the climb, but turned back just 300 vertical feet from the summit when Evans’ oxygen system failed. Hunt then directed Hillary and Norgay to attempt the summit. Snow and wind delayed them on the South Col for two days before they set out on May 28th. The two pitched a tent at 27,900 feet while their support group returned down the mountain. The next day, wearing 30 pound packs and half frozen boots, the two climbers attempted their summit push.

After nearly six hours of trudging up the home stretch of the mountain they reached the final obstacle — the 40 foot rock face now known as the “Hillary Step.” Hillary later wrote:

“I noticed a crack between the rock and the snow sticking to the East Face. I crawled inside and wriggled and jammed my way to the top ... Tenzing slowly joined me and we moved on. I chopped steps over bump after bump, wondering a little desperately where the top could be. Then I saw the ridge ahead dropped away to the north and above me on the right was a rounded snow dome. A few more whacks with my ice-axe and Tenzing and I stood on top of Everest.”

Tenzing Norgay wrote in his 1955 autobiography that Hillary took the first step onto the summit and he followed. They reached the highest point on earth at 11:30am on May 29th, 1953. Spending only 15 minutes at the summit, Hillary took a photo of Norgay posing with his ice-axe, but there is no photo of Hillary. Norgay’s autobiography says that Hillary simply declined to have his picture taken. They were later photographed together upon their return to camp.

By the early-1990’s summiting Mt. Everest had become a booming cottage industry. Just about anyone could do it — as long as they had the money and the time. One of the pioneers of the business, Rob Hall — another mountaineering New Zealander, and the co-founder of Adventure Consultants — had established himself as the “go to” Everest expedition guide after successfully leading thirty-nine, mostly amateur climbers to the summit without incident from 1992 through 1995. This earned Hall a reputation for safety and reliability, allowing him to charge $65,000 per climber for a guided summit attempt — a significant premium to that of other expedition outfitters. Hall’s success also brought him significant respect and several endearing nicknames within the mountaineering community, including the “Mountain Goat” and the “Show.”

As such, the Adventure Consultants 1996 Everest expedition saw strong demand, filling all eight available spots. Hall’s client list for the trek was chock-full of wealthy, middle-aged doctors, but also a few accomplished mountaineers including Japanese climber Yasuko Namba — who had already conquered six of the Seven Summits, and adventure journalist Jon Krakauer, of Outside magazine, and author of the then recent New York Times best-selling book, Into the Wild (Hall had cut a deal with Outside, whereby he would guide one of their writers to the summit in exchange for advertising space and a story about the growing popularity of commercial expeditions to Everest. Krakauer was a proficient technical climber, but had no experience climbing above 8,000 feet). It also included some regular guys, such as Doug Hansen, a postal worker, and amatur climber who had worked a second job and received sponsorship support from his kids’ school in order to to afford the climb in 1995, but the expedition failed to reach the summit then due bad weather. He was back for a second chance in 1996, partially at Rob Hall’s expense.

Hillary, following his Everest summit, went on to climb ten other peaks in the Himalayas from 1956-1965. He also reached the South Pole in 1958 as part of the Commonwealth Trans-Atlantic Expedition, for which he led the New Zealand section. His party was the first to reach the Pole over land since 1912. He further helped organize an expedition in search of the legendary Yeti with fellow adventurer and zoologist Marlin Perkins, of Mutual of Omaha’s Wild Kingdom fame (they found no convincing evidence of the creature’s existence). For all his considerable efforts and contributions to history, Sir Edmund Hillary was appointed Knight Commander of the Order of the British Empire and received the Queen Elizabeth II Coronation Medal, as well as many other awards too numerous to mention. Between Hillary’s exploits and Hall’s success getting his wealthy clients to the summit of Everest, it’s really no wonder why people were lining up in the pursuit of vain glory to pay his $65,000 fee (about $128,500 in today’s dollars).

Tragically for Hall, and seven of the other climbers and guides involved with the 1996 expedition, Mt. Everest would become their final resting place. As Jon Krakauer detailed in his second New York Times best-selling book, Into Thin Air — his personal account of the 1996 Mount Everest disaster — things can go south pretty quickly at 29,000 feet if you fail to respect the risks that exist at that altitude. To be more specific, at about 10,000 feet above sea level, the human body begins to suffer from the effects of hypoxia (aka Acute Mountain Sickness or AMS) — a reduction in oxygen availability, which can impair brain function and motors skills. Between 10,000 and 15,000 feet, brain function is mildly impaired and hypoxic symptoms are common. Above 15,000 feet, brain function exponentially deteriorates with increasing altitude. If altitude is gained too quickly, it can result in the loss of consciousness. For this reason, climbers must first acclimatize before making their ascent on Everest, by setting up camps along the climb, where they must wait for days at a time, and initially weeks at base camp, so that their bodies can adapt to the change in altitude. At altitudes above 26,000 feet — know as the “death zone” — the body literally begins to die, as oxygen levels are insufficient to sustain human life.

In 1996, there was a window between May 8th and May 12th where climbing conditions were expected to be optimal to summit Everest. But, May 10th was the common date that the record number of climbers on the mountain had all chosen. In addition to Rob Hall’s Adventure Consultants expedition, rival Scott Fischer’s Mountain Madness expedition was competing for position on the mountain. There were also the Taiwanese National and Indo-Tibetan Border Police expeditions to compete with for the precious narrow time slot. All in, there were 34 climbers on the mountain all vying to occupy the the same small piece of real estate at the same time. Fischer’s tenacious “go-for-it” reputation created a high potential for a clash of the titans come summit time. But both Hall and Fischer quickly realized that if they each wanted to get their paying clients to the summit of Everest that year, they would all need to work together.

Shortly after midnight on the morning of May 10th, Hall’s Adventure Consultants expedition began its summit attempt from Camp IV, atop the South Col at 25,900 feet. They were joined by six client climbers, three guides, and the sherpas from Fischer’s Mountain Madness expedition, as well as the expeditions sponsored by the governments of Taiwan and India. But, the group quickly encountered delays. The climbing sherpas had not finished setting the fixed ropes by the time the four teams reached the Balcony at 27,400 feet. This cost the climbers almost an hour — waiting in the death zone, consuming their oxygen. Dr. Beck Weathers — one of Hall’s clients, who had undergone radial keratotomy just a month prior to the expedition, became temporarily blinded due the effects of intense exposure to UV radiation so soon after the procedure. What followed is best captured in the 2015 film, Everest, which was loosely based on Krakauer’s book and several other written accounts by survivors. Upon reaching the Hillary Step at 28,740 feet, the climbers again discovered that no fixed lines had been placed, and they were forced to wait for another hour while the guides installed the ropes. As a result, there was a bottleneck at the Hillary Step. The two delays consumed roughly two hours of the oxygen needed above 26,000 feet to reach the summit, and some of the climbers had nearly depleted their tanks. Fortuitously, several of Hall’s clients were forced to turn back and return to Camp IV.

While renown veteran climbers Reinhold Messner and Peter Habeler had proved that it was possible to summit Everest without the use of oxygen back in 1978, the rest of the mountaineering community considered their feat to be sheer lunacy. Only two climbers on the May 1996 expedition were experienced at climbing in such high altitudes without oxygen — Fischer and Anatoli Boukreev, the Russian guide from the Mountain Madness team. Since Boukreev was the one installing the ropes at the Hillary Step along with Andy Harris — a guide on the Adventure Consultants team, he was also the first to reach the summit. After a brief celebration, Boukreev then moved down the mountain with the intention of retrieving additional oxygen tanks to replenish the team’s supply for the descent. Fischer was at the back of the column as the “Sweep.” He had already succumbed to AMS and was in need of additional oxygen even before he made it to the summit. But, by the time he got to Fischer, Boukreev had already given his own supplementary oxygen to a client whose tank was empty. Meanwhile, the weather below was changing rapidly. Reports of an impending storm front slated for May 11th had been distributed to both Hall and Fischer days prior to their summit push, but neither could have known that the blizzard, which hit in full force on the 11th, would be preceded by increasingly high winds and snow during the afternoon and evening hours of May 10th.

Krakauer, who was the third climber to reach the summit that day behind Harris, and who was also running low on oxygen, stayed only a few minutes on top before he began his descent. He would later chronicle the event this way:

“When I reached the summit of Mt. Everest in the early afternoon of May 10, 1996, I hadn’t slept in fifty-seven hours and was reeling from the brain-altering effects of oxygen depletion. As I turned to begin my long, dangerous descent from 29,028 feet, twenty other climbers were still pushing doggedly toward the top. No one had noticed that the sky had begun to fill with clouds. Six hours later and 3,000 feet lower, in 70-knot winds and blinding snow, I collapsed in my tent, freezing, hallucinating from exhaustion and hypoxia, but safe.”

The following morning he learned that six of his fellow climbers hadn’t made it back to their camp and were in a desperate struggle for their lives. When the storm finally passed, five of them would be dead, including Hall and Fischer, and the sixth (Beck Weathers) so horribly frostbitten that both of his hands and his nose would have to be amputated. Three members of the Indo-Tibetan expedition also perished in the storm.

The 1996 Mt. Everest disaster can probably be best attributed to human error — mostly bad judgement on the part of leadership. Delays and bottlenecks impelled the team leader’s collective decision to exceed the planned 14:00 hours turnaround time, with many summitting after 14:30. That, coupled with the sudden illness of two climbers (Doug Hansen and Scott Fischer) near the summit after 15:00 hours due to severe oxygen deprivation, and insufficient stores of reserve oxygen, all set the wheels in motion for what became a tragic ending to an otherwise questionable pursuit to begin with (Fischer may have suffered a High Altitude Pulmonary Edema). The sudden drop in barometric pressure sealed their fate. But in the end, it appears that hubris led to their demise. Some readers may now understand where we are going with all of this. Others may be saying to themselves, “Yeah, so what’s your point?” Our point is this: To understand what it is about Everest that has compelled so many people to throw caution to the wind, ignore all the warnings, and willingly subject themselves to such risk, hardship, and expense is a kin to earning a Ph.D. in human social behavior.

Both the S&P 500 Equal-Weight and the Nasdaq 100 Equal-Weight indexes have advanced by +26.7% in just 105 days from their October lows to their March highs. But bottom-up FTM S&P op-EPS estimates actually contracted by -1.8% during the same period. The entirety of the gain in the stock market over the past five months can be attributed to P/E multiple expansion. The underlying fundamental expectations for those 500 companies actually deteriorated. The change in stock prices reflects a change in investor sentiment. That sentiment shift has been steadily driven to new extremes of optimism during the period — the result of a change in tone by monetary policy makers with respect to the timing of interest rate cuts. The rise in stock prices has in turn caused those whose job it is to explain such changes to further build upon the so-called “soft landing” narrative, adding new fuel to the fire with hopes that cost cutting and productivity improvements from technology investments in artificial intelligence infrastructure will drive EPS growth of 9.1% in 2024 and 13.7% in 2025 (a historically rare feat to be sure — and rarer still given the law of large numbers). Of course, these are not promises. They’re just estimates. Estimates that are subject to change, and are often too aggressive initially (based upon data from 1980-2016, Yardeni Research concluded that the consensus overestimated S&P op-EPS 78% of the time, by an average of +19.0%, as discussed in last month’s issue).

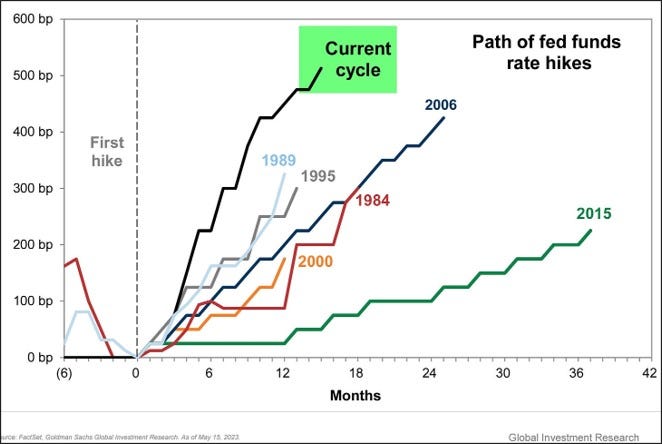

Stock market valuations have ascended too rapidly. Investors are now in the death zone and they don’t even know it. Metaphorically, they are suffering from the effects of hypoxia. They have climbed above 26,000 feet without the benefit a supplementary oxygen. Some have been here before. They are — for all practical purposes — “experienced,” like Fischer and Boukreev. Many more are here for the first time. Some are even “proficient technical climbers,” like Krakauer, Harris, and Yasuko Namba. But most are amateurs, like Beck Weathers and Doug Hansen. Holding stocks when they are priced for perfection is a kin to attempting to reach the summit of Everest during the narrow window when conditions are optimal, despite knowing that a storm is coming. To do it requires something beyond skill and confidence. It requires arrogance, vanity, a need for grandiosity. How will investors fare in the death zone if something goes wrong? Experience and technical proficiency did not help Scott Fischer, Andy Harris, or Yasuko Namba. Even Rob Hall, the “Show” himself, went the way of Long-Term Capital Management when problems arose in the death zone. In August 2015, retrospectively, Jon Krakauer had this to say to the Huffington Post about his experience:

“Climbing Mt. Everest was the biggest mistake I’ve ever made in my life. I wish I’d never gone.”

Beck Weathers lost both hands and his nose in the death zone. So far this year, Tesla shareholders have only lost about one-third of their wealth. As investors succumb to the temptations of vain glory, the altitude leads to hypoxia (aka FOMO) and impairs their judgement. But just how high into the clouds are they now?

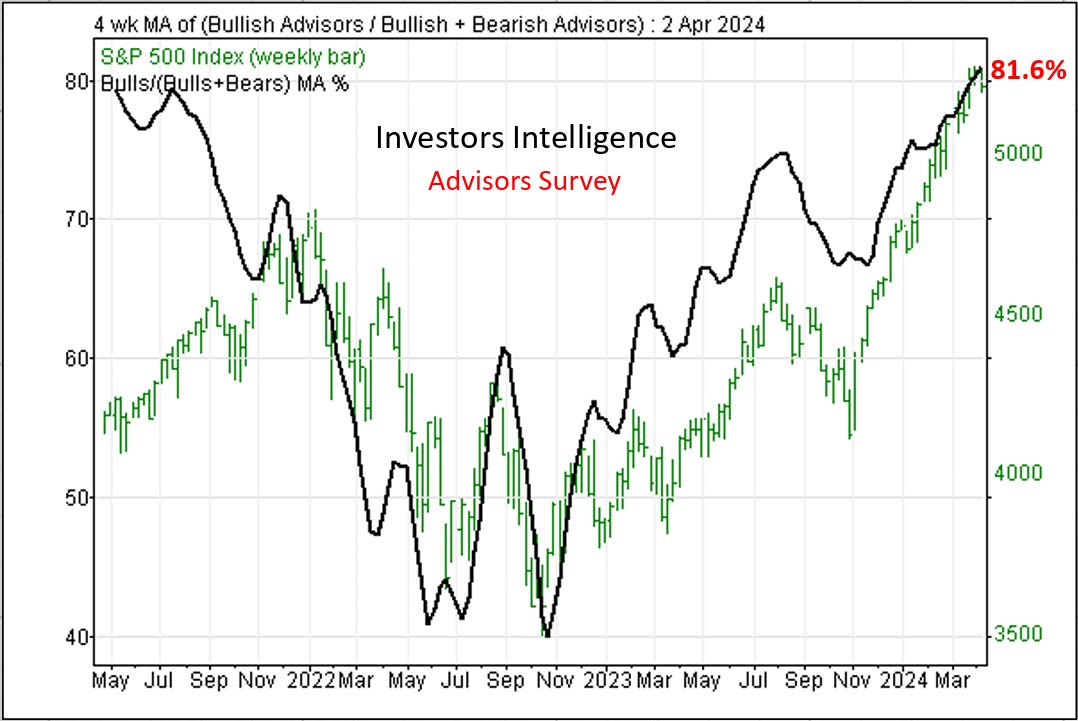

The latest Investors Intelligence Advisors Sentiment Survey of publishing investment strategists has reached a new 3-year extreme of committed bulls. We say committed bulls, because we exclude those advisors who are neutral or expecting a correction [Bulls / (Bulls + Bears)]. That measure has reached 81.6% — the highest level since April 2021. Moreover, the percentage of Bulls not only reached a new extreme of 62.5%, but the sheer absence of Bears at just 14.1% — the lowest level since January 2018, and just shy of a 32-year low — implies that professional advisors are more committed to stocks today than they have been in decades. Indeed, the Bull-Bear spread has now reached 48.4%, the second highest level in the 37-year history of the data, just behind the Dot-Com bubble peak.

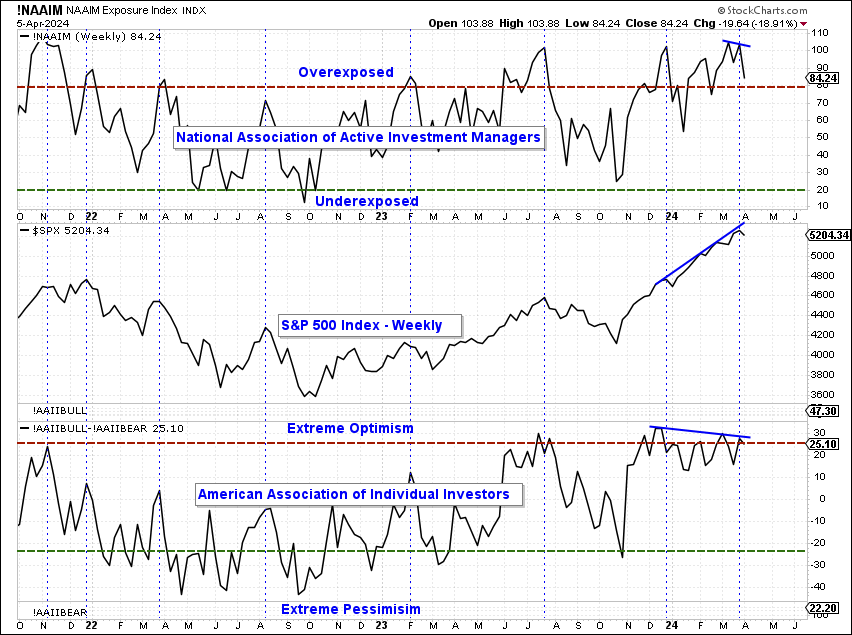

Moreover, the NAAIM Exposure Index of professional investment managers saw its ranks hit 104.8% and 103.9% net equity exposure (a slight negative divergence) in the preceding two weeks prior to falling by nearly 20 percentage points this week. In addition, the results from the latest weekly AAII sentiment survey saw the number of individual investors describing themselves as bullish slip to 47.3% from 50%, while those describing themselves as bearish ticked-down to 22.2% from 22.4% in the prior week. As a result, the Bull-Bear spread slipped two percentage points to form another lower high at 25.1%, sustaining a double negative divergence, since posting two back-to-back weeks at 32% in mid-December. The failure of sentiment measures to confirm price can oftentimes signal the point of recognition among the wisest investors.

The magazine covers above make it pretty clear where the media stands in all of this. Over the past month, two prominent financial periodicals, The Economist and Barron’s, have both featured cover stories that suggest an overwhelming degree of optimism among investors. Normally, a bullish or bearish cover on one of these two publications could be hit or miss, but the fact that they are both emphasizing their optimism in synchronicity, strongly increases the odds of a hit in our experience.

The Euphoriameter, created by Callum Thomas of Top Down Charts, combines the forward 12-month P/E, and the VIX, with bullish sentiment. It reflects that conditions currently emulate those which existed at the 2021 speculative peak, and at the heights of the Dot-Com bubble. While no definitive conclusions can be drawn from any of these measures alone, by combining several independent variables, the Euphoriameter can achieve a sort of triangulation between valuation, positioning, and conviction. The inference is that investors should be wary of forward equity return potential given the neighborhood from which these combined conditions place the current cycle.

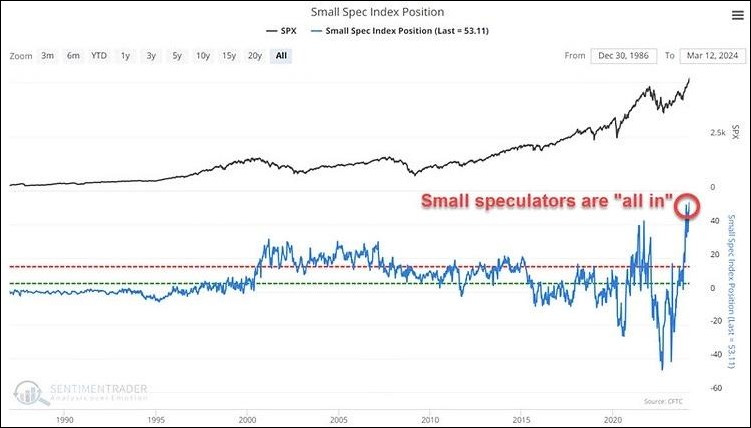

As we’ve been discussing, investor sentiment among HNW individuals, professional investors, and investment advisors has reached new multi-year extremes. But even the little guy has gotten in on the action as of late. The chart above illustrates that the combined net long equity positioning of small traders across all contract sizes in S&P 500, Nasdaq 100, and DJIA index futures has also reached a new all-time record extreme going back to the inception of the data series in 1985. The current level of net bullish positioning at $54 billion now far exceeds all prior extremes such as those seen in 2000-2001 during the Dot-Com mania, 2007 before the GFC, or late-2021 before the markets topped in early-2022.

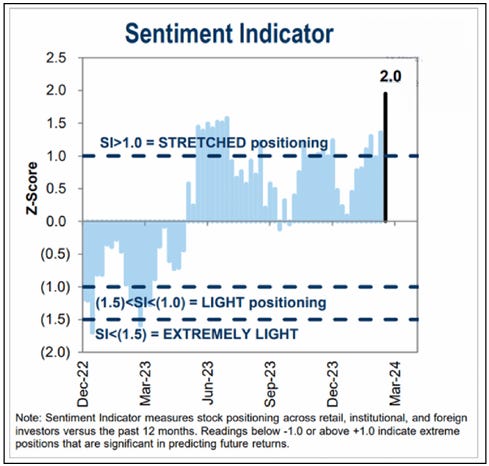

The Goldman Sachs Sentiment Indicator attempts to gauge investor sentiment based upon the net long equity positioning among all investors. The scale measures z-scores over the past 12-month historical period. Since at least December 2022, the current net long exposure of all investors has reached a new relative extreme of +2.0 standard deviations above the historical mean. A reading this extreme is typical during periods when investors are forced to chase performance. Normally, a z-score of +1.0 standard deviation above the mean indicates that net long positioning is sufficiently stretched to predict sub-standard forward returns. Performance chasing fuels the momentum trade, which has now become quite crowded.

But, momentum crowding is a condition that tends to coincide with market tops and often times, near extremes, that condition precedes recessions. Today, according to JP Morgan Equity Macro Research, momentum crowding is near a record high in the 99.8 percentile. This was last seen leading up to the GFC, and before that at the peak of the Dot-Com bubble. They say a bell never goes off at the top, but the signs are everywhere today. With equity investor positioning also reaching new extremes, an inevitable momentum reversal appears likely in our view.

The problem that arises for otherwise rational investors is that they can’t let go at the top. Professional investors have just done too much work, written too many reports, and spent too much time defending their position, that when they finally reach the death zone — and the time comes to sell — they are hallucinating from hypoxia and exhaustion and they think that it’s safer to hold on to what they already know. Daniel Kahneman referred to this emotional bias that places a higher value on an object that is already owned, than on the same object if it were not already owned, as the “endowment effect.” Today, AAPL is one of the most widely held stocks on the planet. We observe analysts and portfolio managers defending the stock daily in the financial media. Few, if any, have acknowledged the fact that the stock has definitively broken below a 5-year structural uptrend off its 2020 low. Most are unaware of the classic patterned “Double Top” formation that has been developing over the past year. None have commited to sell the stock if it breaches key support at $167.

Back in our Merrill Lynch days, circa late-1999, we heard a number of our top institutional clients profess that they knew how overvalued the tech sector was, especially the four horsemen of the Nasdaq (CSCO, MSFT, INTC, and DELL), but they all said the same thing when we called them out on it. “Jeff,” they said, “I’ve been doing this along time. The best growth stocks always look expensive. But you can grow into a multiple pretty quickly when your earnings are doubling every two years.” They all told us that they knew the risks of overstaying their welcome, and that they were certain that they would not be the last drunk at the party. They all assured us that they would sell well-before the bottom fell out. “There’s always time,” they’d say, “Transformational themes unwind slowly.” None of them sold. Most road the four horsemen straight into the October 2002 lows. Few had jobs the following year.

A Prelude to Recession

Inflation pressures are abating, but the Fed’s goal of 2.0% appears allusive. Recent data suggest that core inflation remains sticky, especially in housing and services. Monetary policymakers have historically used or monitored various measures of underlying inflation to gain context about longer-term trends. The Atlanta Fed’s Inflation Dashboard is a tool that provides a nice comparative analysis of the various measures. The Fed gets a broader characterization of retail price pressures from this dashboard than by monitoring movements in core PCE alone. While none of the nine measures is still printing above levels that prevailed a year ago, the current message from the dashboard is that core inflation is still 173 bps above target. As such, in our view, it is unlikely that the Fed will begin cutting rates in the first half of 2024 —barring a crisis, or convincing evidence of an impending recession.

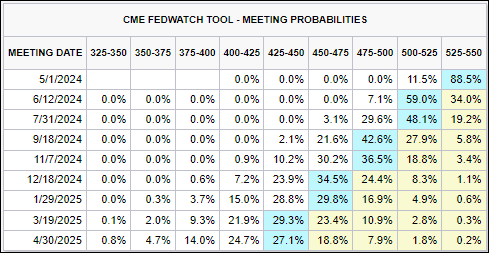

The monetary policy environment has shifted dramatically since March 2022, from a 13-year period of aggressive accommodation, to one that is now relatively restrictive. The Fed raised its funds rate eleven times over the past 24-months by a total of 525 bps. However, the consensus view has shifted to reflect a 59.0% probability that the Fed will begin reversing this process at the June 12th FOMC meeting, despite repeated warnings to the contrary from the Fed Chairman and many voting committee members in recent days. We think that the Fed is dancing on a razor’s edge. With Powell’s legacy at stake, we doubt that the Fed is seriously considering a rate cut in the first half of the year. However, if the economy enters recession by 2Q24 as we suspect it will, then we do think that possibility could emerge. We monitor five economic models that inform our recession forecast. Four of those models have been blinking red for the the better part of the last 18-months, but to no avail, thus far. The fifth had been neutral, but was put on negative watch for a downgrade in March.

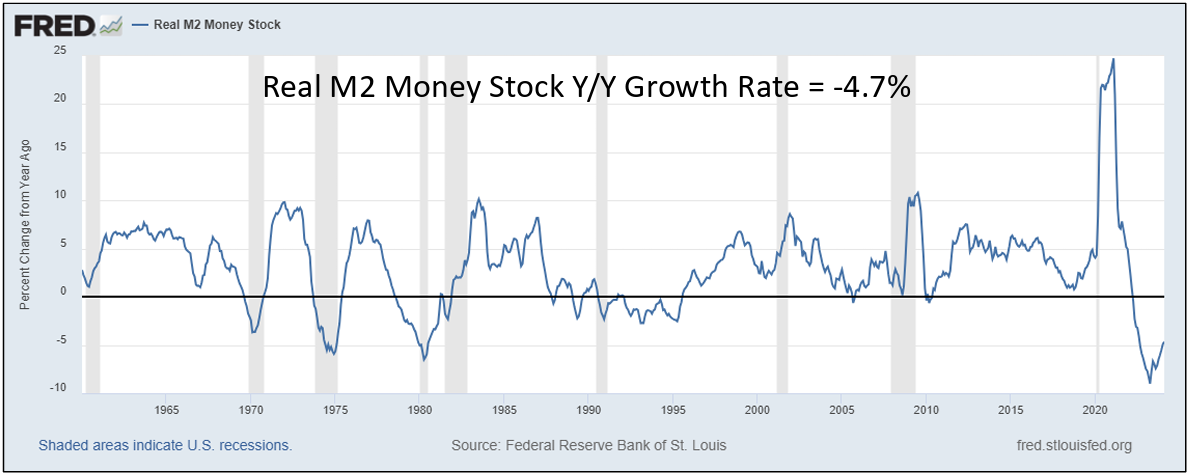

Recession Model #1 - Liquidity: Although the Real M2 Money Stock in the U.S. (reported monthly w/ a 30-day lag) has further improved since the record April low to end the month of February down -4.7% Y/Y. It has been negative for the past 24-months — the second longest period of contraction on record. The data series goes back to January 1960. Prior to November 2022, the lowest print in the history of the data was -6.5%, which occurred in April 1980, in the midst of the first of two back-to-back recessions in the early 1980s — then widely considered to be the two worst recessions in U.S. since the great depression. Why have financial conditions loosened if real M2 growth remains negative? The answer is that the Fed’s Reverse Repo Facility has been drained by approximately $1.85 trillion over the past year — offsetting the Y/Y decline in real M2. But that facility has now dwindled down to just $440.5 billion. Risk Assessment: High

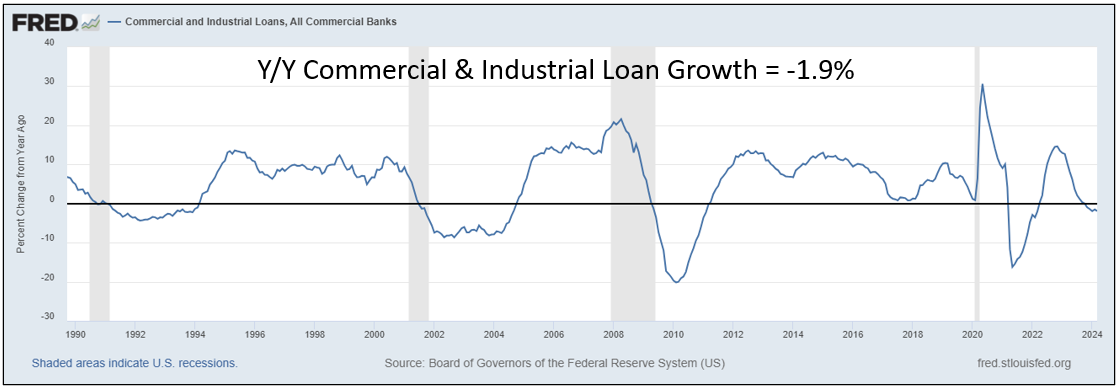

Recession Model #2 - Bank Credit: The widely discussed, impending credit crunch has already arrived and appears to be in full-swing. While just 14.5% of loan officers still see a tightening of credit and lending standards for C&I loans, according to the latest quarterly U.S. Senior Loan Officers Opinion Survey, the growth of new commercial and industrial loans has contracted for a 5th consecutive month in March by a rate of -1.9% Y/Y. This has never happened before in the history of the data without preceding, or being attended by a concomitant U.S. economic recession. As money continues to seek higher yields, bankers have been attempting to stem the tide by offering competitive yields on Jumbo CDs, but depositors appear to be walking nonetheless, in order to move their cash from demand deposit accounts to higher yielding money market accounts and T-Bills where short maturity securities offer safety, liquidity, and yields of up to 5.43%. To be sure, riskier collateral and the decline in funding sources are tightening lending standards, but the rise in borrowing costs have curtailed new loan demand as well. Risk Assessment: High

Recession Model #3 - LEI Index: The LEI has a 100% hit rate when it comes to anticipating recessions. The trigger occurs when the LEI declines for at least two consecutive months. This most recently occurred 19-months ago in August 2022 and has remained negative ever since. Based upon data going back to 1970, the lead time to recession has ranged from 6 to 8-months. The Conference Board’s Leading