HUGE INSIGHTS: The Big Picture - Issue #20

HUGE INSIGHTS: The Big Picture - Issue #20

This is No Joke!

Please enjoy the free portion of this monthly newsletter with our compliments. To get full access, you might want to consider an upgrade to paid for as little as $10/month. As an added bonus, paid subscribers also receive our weekly ALPHA INSIGHTS: Idea Generator Lab publication, which details our top actionable trade idea and provides updated market analysis every Wednesday, as well as other random perks, including periodic ALPHA INSIGHTS: Interim Bulletin reports and quarterly video content.

The recent failures Silicon Valley Bank (SVB) and Signature Bank of NY, not to mention the shotgun wedding in Switzerland between Credit Suisse and UBS, have put the incompetence of central bankers on full display. First, they overstimulated the system resulting in a tsunami of inflation, the likes of which had not witnessed since the Carter administration. Next, they ignored obvious evidence that inflation had reared its ugly head, while continuing their dovish policy exploits to appease political agendas, not to mention their egos — adding fuel to the fire — allowing it to get out of control. Then they toyed with it by raising rates only modestly, before it became clear that their attempts at restraining the beast had been futile. Finally, they beat it unmercifully, in an attempt to “show it who was boss,” without any regard for the unanticipated consequences of their actions, or the potential for collateral damage.

The resulting spike in interest rates has led to a collapse in housing activity — with affordability now at a record low — leaving millions of families trapped and unable to sell or access the equity in their homes; an unfathomable duration mismatch between bank assets and liabilities, which could pose an existential threat to an otherwise well-functioning banking system; and now, a seismic credit crunch that has the potential to grind the wheels of global commerce to a halt.

The Fed is made up of academics and is run by a lawyer. This cohort of regulators thinks about conditions in a vacuum. For example, “all else being equal, a change in interest rates has the opposite effect on production — in due course.” They implement policy in a manner that suggests little more than a process of trial and error, and as if they could easily correct the outcome of their decisions by taking an eraser to a blackboard. Unfortunately, it doesn’t work that way in the real world. What’s done is done. Once the wheels are in motion you own those results — whatever they may be.

So far, central banker’s policy actions have exposed at least three pockets of gross mismanagement in the banking system. The first serious bank run since the collapse of Washington Mutual in 2008, forced banks to borrow a combined $164.8 billion from two key Fed backstop facilities in the week following the SVB collapse, a sign that funding strains have escalated. Usage of the discount window, the Fed’s traditional liquidity backstop for banks, accounted for $152.85 billion of that — significantly above the prior record amount of $111 billion during 2008. The central bank’s newest backstop, the Bank Term Funding Program, provided $11.9 billion in funds during its first week of operation. Meanwhile, other credit extensions totaled $142.8 billion during the week, which reflects lending by the Federal Deposit Insurance Corporation (FDIC) to the bridge banks for SVB and Signature Bank. As Warren Buffett once put it, “only when the tide goes out do you discover who’s been swimming naked.” The question that remains is — who’s next?

The Road to Serfdom

According to a recent paper entitled, Why do banks invest in MBS?, published by researchers at New York University and the Wharton School (Schnabel, Savov, and Drechsler — March 13, 2023), U.S. banks had unrealized losses of $1.7 trillion on their held-to-maturity (HTM) portfolios at the end of 2022. At that time, the losses were rapidly approaching the banks’ total equity of $2.1 trillion. Rising interest rates have slashed the value of the U.S. Treasury and mortgage-backed securities that make up a large portion of the HTM assets at many banks. Moreover, bank deposits fell by nearly $100 billion during the week ended March 15th according to data released by the Federal Reserve.

Many bank depositors moved their accounts to the large, so-called systemically important financial institutions (SIFI), as savers and CFOs alike suddenly lost confidence in some of the nation’s heretofore well-regarded regional and community banks. Indeed the St. Louis Fed Financial Stress Index reached a level exceeded on only four other occasions in its history including the COVID pandemic in 2020, the great financial crisis (GFC) in 2008, the terrorist attacks on 9/11 in 2001, and the Long-Term Capital Management melt-down in 1998.

Of course, regulators have spent the last two weeks reassuring the public that the banking system is safe. On Friday, March 15th, Treasury Secretary Janet Yellen and Federal Reserve Chairman Jerome Powell, along with dozens of other officials convened a special closed meeting of the Financial Stability Oversight Council. After the markets had closed for the week, the group released a statement that read, “The Council discussed current conditions in the banking sector and noted that while some institutions have come under stress, the U.S. banking system remains sound and resilient.” There were no other details provided on the meeting. Yet, we question exactly how that could be true, given the extent to which small bank balance sheets are laden with distressed commercial real estate loans.

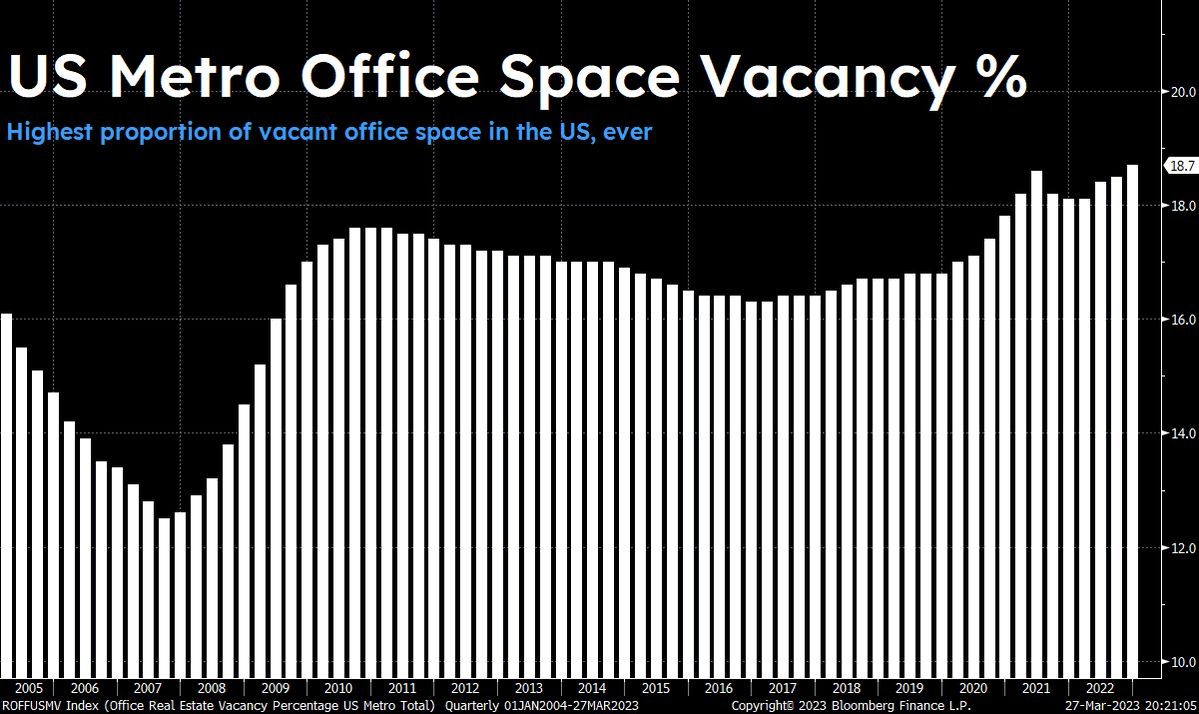

Small U.S. banks currently hold approximately 70% of all commercial real estate loans. Of that, office properties account for roughly 60% of the underlying collateral for the more than $3 trillion in CRE loans on the books of these small banks. According to Bloomberg, as of March 27th, U.S. metropolitan office space vacancy rates have grown to an average of 18.7%, the highest level in the history of the data. That’s more that a full percentage point above the 2010 post-GFC peak, and supposedly, we aren’t even in a crisis yet? The problem is that weak fundamentals have put severe pressure on property owner’s net operating income, which in turn has resulted in an increase in delinquent loans. According to data from Trepp, the CMBS delinquency rate for office properties jumped 55 bps M/M in February to an average of 2.38%. Worse yet, the proportion of CMBS loans that have moved into the “workout” stage also climbed by 60 bps to 4.43%. With over $450 billion in CRE loans set to mature in 2023 alone — according to J.P. Morgan, these undercurrents of financial stress now threaten a new wave of defaults.

Another paper on the subject entitled, Monetary Tightening and U.S. Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?, published by economists from USC, Northwestern, Columbia, and Stanford (Jiang, Matvos, Piskorski, and Seru - March 13, 2023), reveals that 186 banks are at risk of “impairment” of $300 billion worth of insured deposits. And if uninsured deposit withdrawals cause even small fire sales, substantially more banks are at risk. The authors’ calculations suggest that recent declines in bank asset values have very significantly increased the fragility of the U.S. banking system.

It is certainly not our intention to instill fear and doubt into the minds of our readers with respect to the stability and reliability of the U.S. banking system, but just to advise a healthy dose of skepticism. You simply can’t take the word of government officials at face value during a crisis. They’re only going to tell you what they want you to hear. The same can be said for the managements of the banks. For example, it’s an indisputable fact that the management of SBV received six warnings from the Federal Reserve about the financial risks on their balance sheet beginning as far back as October 2021. In addition, Moody’s warned SBV’s management of an imminent downgrade just one month before it announced its emergency capital raise. Yet, SVB’s management made no effort to convey this information to its shareholders.

When we started our career in the investment business back in 1990, it was right in the eye-of-the-storm that became known as the “Savings & Loan Crisis.” But the problems affecting the S&L industry eventually infected the entire U.S. banking system as outlined in a comprehensive examination published by the FDIC entitled, The Banking Crises of the 1980s and Early 1990s: Summary and Implications. Indeed, between 1980 and 1994, more than 1,600 financial institutions received FDIC assistance, far more than in any other period since the advent of federal deposit insurance in the 1930s. Because the Federal Savings and Loan Insurance Corporation (FSLIC) was hopelessly undercapitalized, the FDIC was forced to absorb the FSLIC’s liabilities in order to stabilize the system. Ultimately, just under 300 banks and S&Ls were permanently closed and their assets seized and auctioned off by the newly created Resolution Trust Corporation.

A post-mortem analysis of the crisis by the FDIC’s Division of Research and Statistics determined that there was no single cause, or even short list of causes. Rather it found that it resulted from a concurrence of various forces working together to produce a decade of banking crises. The lessons that can be gleaned from the rise in the number of bank failures in the 1980s is that: 1) Broad national forces – economic, financial, legislative, and regulatory – established the preconditions necessary for the failures; 2) A series of severe regional and sectoral recessions hit banks in a number of markets; and 3) Some of the banks in these markets assumed excessive risks and were insufficiently restrained by supervisory authorities. Does any of this sound familiar? With history as our guide, it’s our opinion that the show is now just getting started folks — caveat emptor!

On the international front, the situation may be even worse. Following the impromptu merger between Credit Suisse and UBS, which led the Swiss National Bank to force a default on the former’s additional tier 1 (AT1) debt, credit default swap (CDS) rates — the cost to insure against default — for UBS’s debt jumped by just under 100 bps, but that was nothing compared to the move in CDS rates on Deutsche Bank’s 1-year subordinated debt, which have soared by nearly 800 bps since the banking crisis began. Remember, a bear market will always call your bluff — one way, or another!

We see one of two possible outcomes to the situation at hand: 1) A new era of tighter